Too much money, burning a hole in your current account?

Not necessarily a common problem, but if you haven’t already invested it somewhere, how do you make your money work for you? You don’t want it just sitting in a current account or savings account losing value to inflation.

An obvious first port of call might be stocks or the now trendy crypto. However both offer large amounts of volatility (variation in price) and it’s hard to predict when is a good time to buy. As Muslims we try and avoid interest/usury/riba, meaning we can’t just leave our money in a savings account to gain money through interest. Spiritually speaking this would be disease, and financially speaking it would just be unwise; given the comparatively low interest rates compared to inflation.

Index Funds – A Word From The Professionals

Index funds are one of the easiest things to invest in long-term. The aim is to make sure your savings at least keep up with inflation and statistically beat it. Recommended by many including, Warren Buffett, one of the richest and most successful investors of the last a hundred years.

“Index funds are the answer for most investors. The fact that it’s so hard to predict what kind of tremendous change there will be in the world is a great argument for diversified index funds, Buffett said.” – Via Bloomberg

“The billionaire has advised the trustee of his will that when he passes, 90% of his bequest to his wife — now in Berkshire stock — should be in a stock index fund like the S&P 500, and 10% in Treasury bills.” – Via Bloomberg

Index funds are an easy place to lock your money away and watch it gain slow but steady returns. These should compound over time to give you some strong holdings when you need them further down the road.

“One of the best arguments for an … index fund is that it beats most fund managers most of the time and the fees are usually close to zero.” — Forbes

When you invest in an index-fund you’re investing in a basket-of-stocks. As such you’re not just investing in one company but many. That is to say you’re investing in a diversified portfolio. (Similarly ETF’s also offer you a way to invest in a wide range of assets through one simple investment).

A good example of an index fund is the Vanguard “FTSE 100 Index Unit Trust” which tracks the performance of the 100 largest companies in the UK.

This has the benefit that if one stock falls in value, your overall holdings are diversified and won’t fall as much as that individual stock. There’s no getting around the fact that if the majority of your portfolio takes a loss at the same time you will incur overall losses, but a well diversified portfolio should be better prepared to weather smaller variations. A diversified portfolio like this should expect to see steady growth over the long term.

Halal Index Funds?

Given that index-funds track a basket-of-stocks, it is worth checking what some of those stocks are. For example the FTSE-100 includes some of the largest companies in the UK, but are these all ethical companies that we would want to be invested in? Some of them may be involved in business we find unpalatable or outright haram.

Without getting into too many of the details, there are halal index-funds out there offered by major players such as iShares and HSBC. In terms of indices, iShares offer a couple of indices that each track the performance of key companies in different regions. To quote the literature from iShares on their Emerging Markets Islamic fund:

“The Index measures the performance of the Shari’ah compliant equity securities in large and mid capitalisation companies in emerging markets determined to be compliant with Shari’ah principles by the Index provider’s Shari’ah panel.”

To summarise: they only invest in companies that are in-line with the Islamic ethics agreed upon by their shariah board.

They offer three main indices, each focusing on different markets:

- ISDE – iShares MSCI EM Islamic – Emerging markets

- ISWD – iShares MSCI World Islamic – Developed countries

- ISUS – iShares MSCI USA Islamic – USA 🇺🇸

HSBC also offer an Islamic fund. Similar to the iShares funds, the fund invests in companies in a way that “meet[s] Islamic investment principles”. At the time of writing this fund mostly holds tech so is also a great way to gain exposure to FANGMA companies.

For a more complete list of Islamic Index Funds please check out Islamic Finance Guru (IFG). https://www.islamicfinanceguru.com/investment/full-list-of-islamic-equity-funds-islamic-mutual-funds/

(Brief aside) Tech stocks

On the subject of tech I’ll briefly mention Evolve’s FANGMA ETF. That allows you to gain exposure to all the major FANGMA companies: Facebook, Amazon, Netflix, Google, Microsoft, Apple. Without having to buy individual stocks of each company.

“Currently, high share prices may deter investors from adding all of these companies individually to a portfolio. With the Evolve FANGMA Index ETF investors get exposure to all six companies for a reasonable unit price. Make investing in big TECH easy.” – Evolve

Tech stocks have been great performers in recent years and it must be fun knowing you own a little piece of Netflix, not just a monthly subscription!

That being said individual tech stocks have become quite expensive individually. If however you have the money up-front you could consider investing directly into a few stocks using a low-fee platform such as Degiro. Checkout IFG for a comparison of low-fee platforms for buying stocks.

Investing through ISAs

Having touched upon ETF’s and index-funds, how does one actually invest in them? One of the easiest, tax-efficient ways is through an ISA.

ISA’s provide a low-tax way to invest up to 20k(GBP) a year. Please read up on the details here: https://www.gov.uk/individual-savings-accounts/how-isas-work

In short:

You do not pay tax on: income or capital gains from investments in an ISA

The easiest way to setup an ISA is through an ISA provider such as:

- AJ Bell (https://www.youinvest.co.uk/isa)

- Hargreaves Lansdown (https://www.hl.co.uk/partners/search/stocks-shares-isa)

- IG (https://www.ig.com/uk/investments/isa)

Once you have opened an ISA with them and deposited some money, they each offer to sell you shares of an ETF or index-fund that you can invest in. You can do this via a “stocks and shares ISA”. From there you can look for various halal & shariah compliant funds to invest in as mentioned above.

A complete list of Islamic Funds is available here: https://www.islamicfinanceguru.com/investment/full-list-of-islamic-equity-funds-islamic-mutual-funds/

iShares offer the following funds (detailed above):

- ISDE – iShares MSCI EM Islamic – Emerging markets

- ISWD – iShares MSCI World Islamic – Developed countries

- ISUS – iShares MSCI USA Islamic – USA 🇺🇸

And there is also the HSBC Islamic fund: https://www.hl.co.uk/funds/fund-discounts,-prices–and–factsheets/search-results/h/hsbc-islamic-global-equity-index-class-ac-accumulation

Compound Returns

“Compound interest is the Eighth Wonder of the World. He who understands it, earns it; he who doesn’t, pays it for the rest of his life.” — Einstein (maybe)

In short, the more money you invest to begin with and the longer you leave your money to gain returns the larger the end result will be. The crucial point is that the end-result can end up being vastly disproportionate to the initial input!

For some reason we have trouble intuitively predicting the value of compound-returns. It’s the same reason if you’ve ever had to pay interest on a credit card or a mortgage it can just seem to be never ending, even after you’ve paid-off far more than the principal.

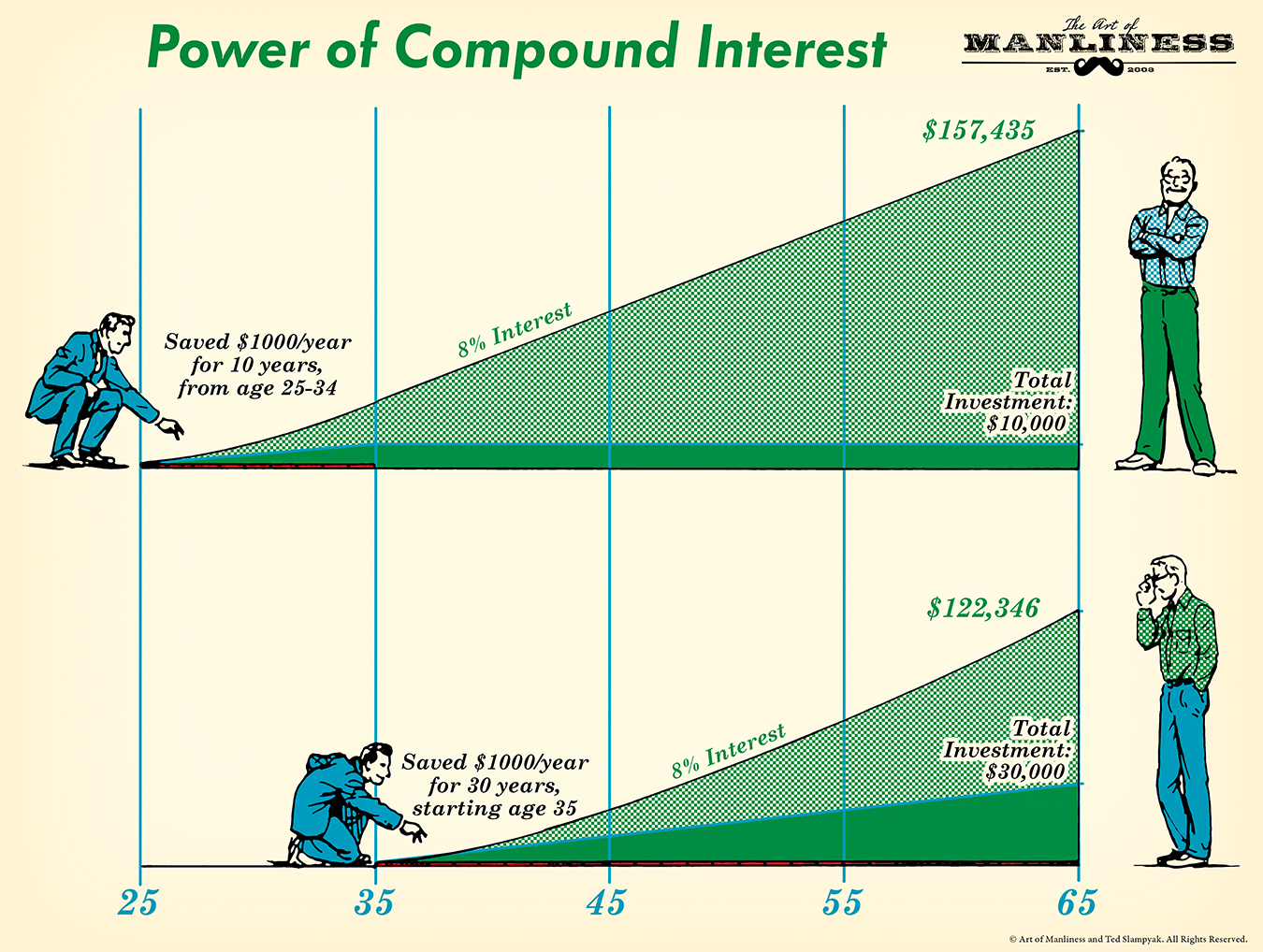

This is mostly clearly highlighted by just running the maths and the numbers on the investment. This can be seen easily in the following diagram (source):

In the first example at the top, the man invests 10 years earlier. And invests on a shorter time-horizon, only investing for 10 years from age 25-34. Whereas the second man starts ten years later, investing at 35, investing for three times as long and three times the value! The second man despite putting in three times the value and time, still ends up with 20% less money!

In short this difference in time (and principal) can lead to a huge difference in your outcomes when it comes to investing. But how do you make sure you benefit from compound-returns and don’t lose out?

The shortest answer I can think of is to make sure you invest as early as possible, with as much up-front as possible. That’s easier said than done, but ideally a little frugality in early years can lead to greater dividends down the line.

Conclusion

Having already said too much, I’ll clarify by saying I’m no expert and I highly suggest turning to the professionals at Islamic-Finance Guru who can offer you some in-depth advice. They’re a great team, providing solid resources around halal investments for beginners and seasoned investors alike.

Further reading:

“How your coffee could be worth £464,000!” A nice intro from IFG covering the basics of long-term investments while also being quite amusing: https://www.youtube.com/watch?v=0Hkpnh9V0jQ

SCOTT GALLOWAY: How to become truly rich (hint: it’s not by trading on Robinhood) – An overall philosophy-of-life piece but also very nicely covers the basics of long-term investments.

Originally published on his blog as “The Algebra of Wealth”: https://www.profgalloway.com/the-algebra-of-wealth/

Some choice quotes:

Re: investing, the long-term is our ally, the short-term our nemesis. …, Albert Einstein, supposedly remarked that compound interest is the eighth wonder of the world. Yet our brains are not wired to understand this. When I was 26, I thought of being 46 as the distant, irrelevant future. Now that I’ve reached that age (actually I’m 56 … ughh), 26 feels as if it was last year. But small investments I made a decade-plus ago have grown into the base of my economic security

Trading — distinct from ‘investing’ — can feel like work and productivity. It’s not. It’s gambling, but without free drinks and with worse odds

In any economic climate, how do we build economic security, foster love, and find joy? How do we get rich? Slowly. Life is so rich

If you’re looking to take a punt on some individual stocks IFG have a great breakdown of different investment platforms. Personally I’ve tried Degiro and find it to be very user-friendly with low-fees.

- (2021) Low-Cost Brokers Compared: T212, M1 Finance, DEGIRO and others: https://www.islamicfinanceguru.com/investment/low-cost-brokers-compared-t212-m1-finance-degiro-and-others/

- (2021) Great example of investing in individual stocks from home – How I Beat The Stock Market by 27% Consistently Over 4 Years: https://www.islamicfinanceguru.com/investment/how-i-beat-the-stock-market-by-27-consistently-over-4-years/

Other potential halal-investments that look beyond just index-funds: https://www.islamicfinanceguru.com/halal-investments/

Intro to some riskier but more lucrative investments: https://www.islamicfinanceguru.com/investment/high-risk-high-reward-investments-how-to-do-them-right/